stETH Liquidity Held Its Ground During the KelpDAO Stress Event

A major external shock tested ETH-denominated liquidity. stETH pricing moved, market depth got more expensive, but the core asset remained functional and resilient.

The April 2026 KelpDAO rsETH exploit was a significant external shock to restaking and ETH-denominated lending markets. This article focuses on secondary-market stETH and wstETH pricing/liquidity during the KelpDAO incident.

It does not assess user outcomes in KelpDAO or EarnETH. The core point is narrower: stETH and wstETH were not the compromised asset path, and market data showed resilience under a significant external shock.

A large external shock, clearly bounded

On April 18, 2026, attackers exploited KelpDAO’s LayerZero-based rsETH bridge path. Public post incident analysis described the event as a cross-chain verification failure: approximately 116,500 rsETH, worth roughly $292 million, was released on Ethereum without a matching source-chain burn. The immediate stress channel was restaking collateral and lending-market exposure, not Lido core staking.

That distinction matters. stETH and wstETH were not directly affected by the KelpDAO incident. Lido internal protocol mechanics functioned exactly as intended and these mechanics did not at all contribute to the market volatility that followed. The protocol also processed one of the largest periods of net outflows in its history. Markets still repriced risk, but participants could distinguish between a failure in a specific cross-chain restaking asset path and the liquidity profile of stETH as Ethereum’s largest liquid staking token. stETH pricing moved, then recovered toward normal levels.

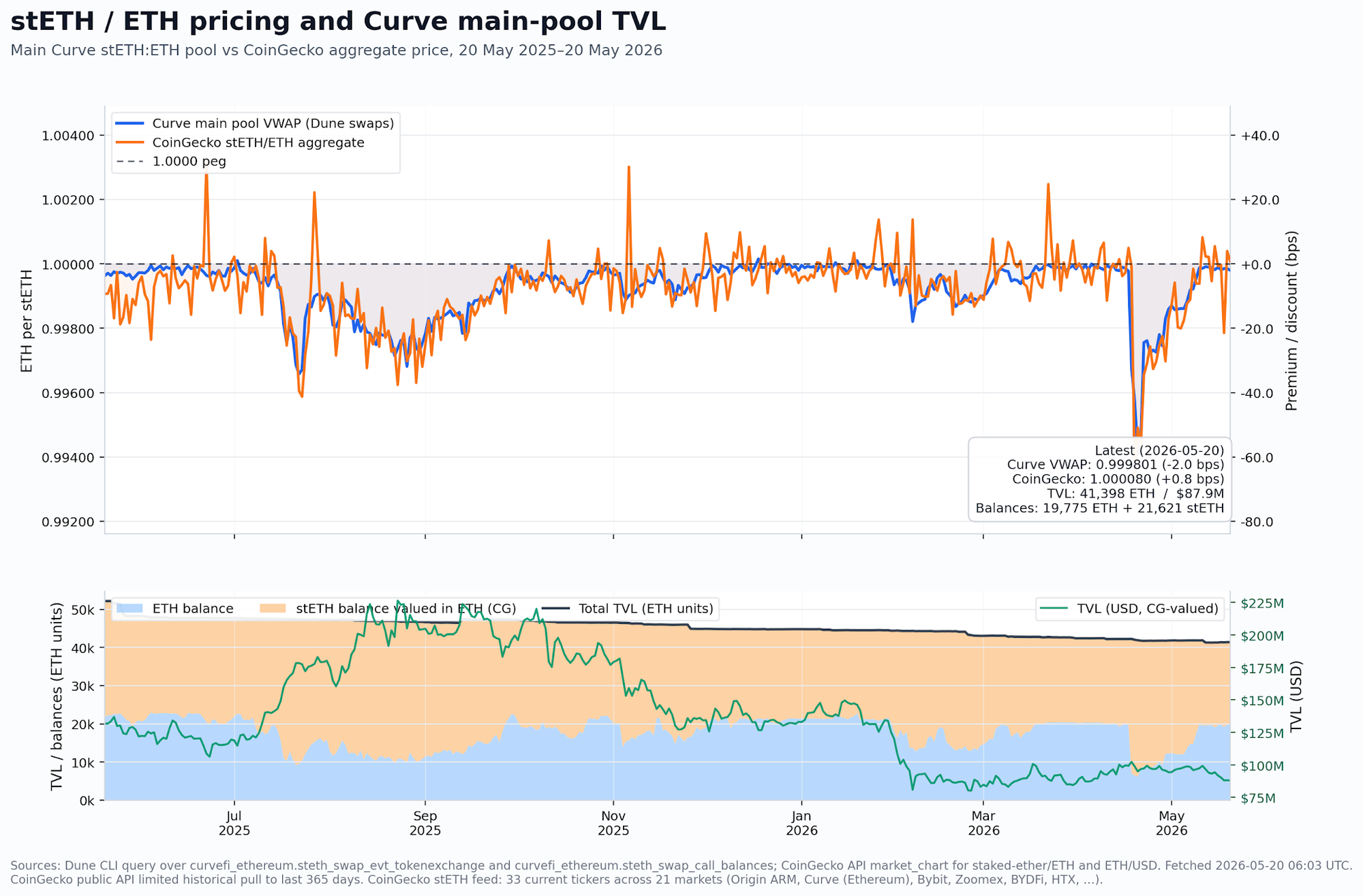

During the April 18 to 28 stress window, Curve main-pool daily VWAP reached a low of approximately 0.9941 ETH per stETH, or about -59 bps versus parity. CoinGecko aggregate stETH/ETH pricing reached a comparable low of approximately 0.9934. By May 20, Curve VWAP was back near parity at 0.99980, with CoinGecko at 1.00008.

Figure 1. stETH/ETH pricing and Curve main-pool TVL. Curve main-pool VWAP is compared with CoinGecko aggregate stETH/ETH pricing; pool TVL and balances are shown below. Sources: Dune and CoinGecko API.

Liquidity depth remained actionable at $1 million notional

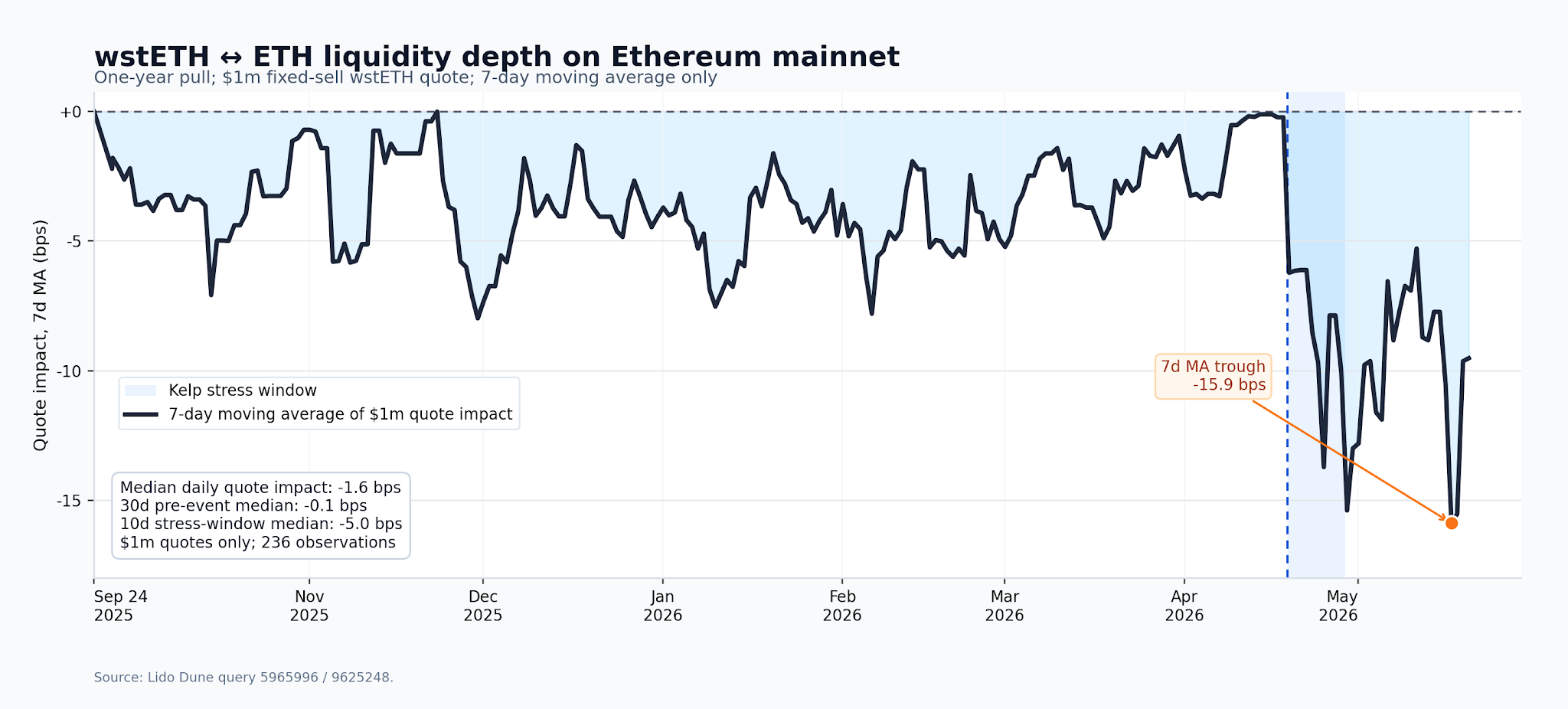

Headline prices can look stable even when execution quality deteriorates. For that reason, liquidity depth is the more useful stress metric. For a $1 million fixed-sell wstETH quote on Ethereum mainnet, the median daily quote impact across 236 observations was -1.6 bps. In the 30 days before the exploit, the median was -0.1 bps. During the 10-day stress window, the median moved to -5.0 bps, and the 7-day moving average reached a trough of -15.9 bps.

That was a real increase in execution cost, but not a disappearance of liquidity. For a major external exploit affecting restaking collateral and lending-market utilization, wstETH/ETH execution remained measurable, routable, and interpretable.

Figure 2. Quote impact for a $1m fixed-sell wstETH quote on Ethereum mainnet, shown as a 7-day moving average across the full Dune query date range. Source: Lido Dune query 5965996 / 9625248.

Why stETH remained comparatively resilient

- Broad venue distribution: stETH and wstETH liquidity is not confined to one pool or one route. Curve is central, but aggregators, RFQ systems, lending venues, market makers, and institutional routing infrastructure all contribute to execution depth.

- Clear risk boundaries: the incident centered on rsETH cross-chain accounting and lending collateral, not the stETH/wstETH asset path.

- Transparent on-chain data: pool balances, DEX trades, routing depth, and secondary prices can be monitored in real time, supporting arbitrage and faster normalization.

- Persistent ETH-denominated demand: stETH remains one of DeFi’s most recognized ETH staking collateral assets, with integrations that support both holding and swapping demand.

The takeaway: resilience where it matters

The KelpDAO incident showed why liquidity must be evaluated under stress, not only in normal conditions. For stETH, the April event showed that deep secondary markets, transparent on-chain pricing, and wide ecosystem integration can absorb a severe external shock without compromising the core staking asset. Pricing moved. Execution cost rose. The market remained functional.

The outcome reflects years of liquidity building around stETH as a foundational Ethereum asset, and it remains a core advantage for users, integrators, and protocols that need staking collateral to be useful not just in quiet markets, but when markets are under pressure.