How Liquid Staking Unlocks Higher Rewards for ETH ETFs and ETPs

Ethereum ETFs and ETPs are emerging as an important institutional channel for accessing ETH exposure. The next divide is between products that capture staking rewards and products that leave them on the table.

More than 30% of ETH is staked across the Ethereum network. WisdomTree launched a 100% stETH-backed European ETP in December 2025, and VanEck filed a preliminary prospectus for a proposed U.S. stETH ETF in October 2025. The issue is no longer whether staking belongs in regulated ETH wrappers, but what form it should take.

The ETF Staking Opportunity

The key challenge in staked ETH products is how to add staking while preserving the liquidity, capital efficiency, and operational predictability participants expect from an exchange-traded product.

A passive ETH wrapper misses out on staking rewards that many institutions increasingly see as part of full ETH exposure. As more ETH is staked across the network, the economic gap between staked and unstaked positions becomes harder to ignore. For ETP issuers, that choice has competitive implications.

Exchange-traded products need daily pricing, reliable liquidity, custody controls, and operational predictability. The priority is choosing the staking approach that best fits those requirements.

Why Native Staking Presents Structural Challenges for ETPs

A natively staked position depends on validator operations, which means liquidity is not always available when the product needs it. New ETH must pass through validator entry, and exits through the withdrawal process. Those delays are variable, but they can become material during periods of higher demand.

In early March 2026, for example, Ethereum’s validator queue showed an entry queue of roughly 57 days, an exit queue of about 1.5 days, and an additional sweep delay of around 8 days.

For an ETF or ETP issuer, this typically presents three possible approaches:

- Keep a meaningful portion of the portfolio unstaked as a liquidity buffer: This reduces the portion of assets actually earning staking rewards. In practice, issuers running natively staked ETPs typically hold 30-40% of assets unstaked to meet redemption requirements. That means a meaningful percentage of the product may sit idle rather than earning staking rewards.

- Stake more of the portfolio and rely on outside liquidity for redemptions: That liquidity may come from market makers, OTC desks, a line of credit, or other financing arrangements. The cost of that liquidity can also increase the product’s total expense ratio.

- Take on a more complex operating model internally: In practice, that means actively managing validators, planning around queue delays, and handling the gap between when investors want liquidity and when staked ETH can actually be withdrawn.

None of these choices makes native staking unworkable, but all add complexity. Native staking may still make sense for institutions that want direct validator control. It is simply less well suited to an exchange-traded product that has to balance staking rewards with liquidity, reliable pricing, and operational simplicity.

Liquid Staking as an Infrastructure Alternative

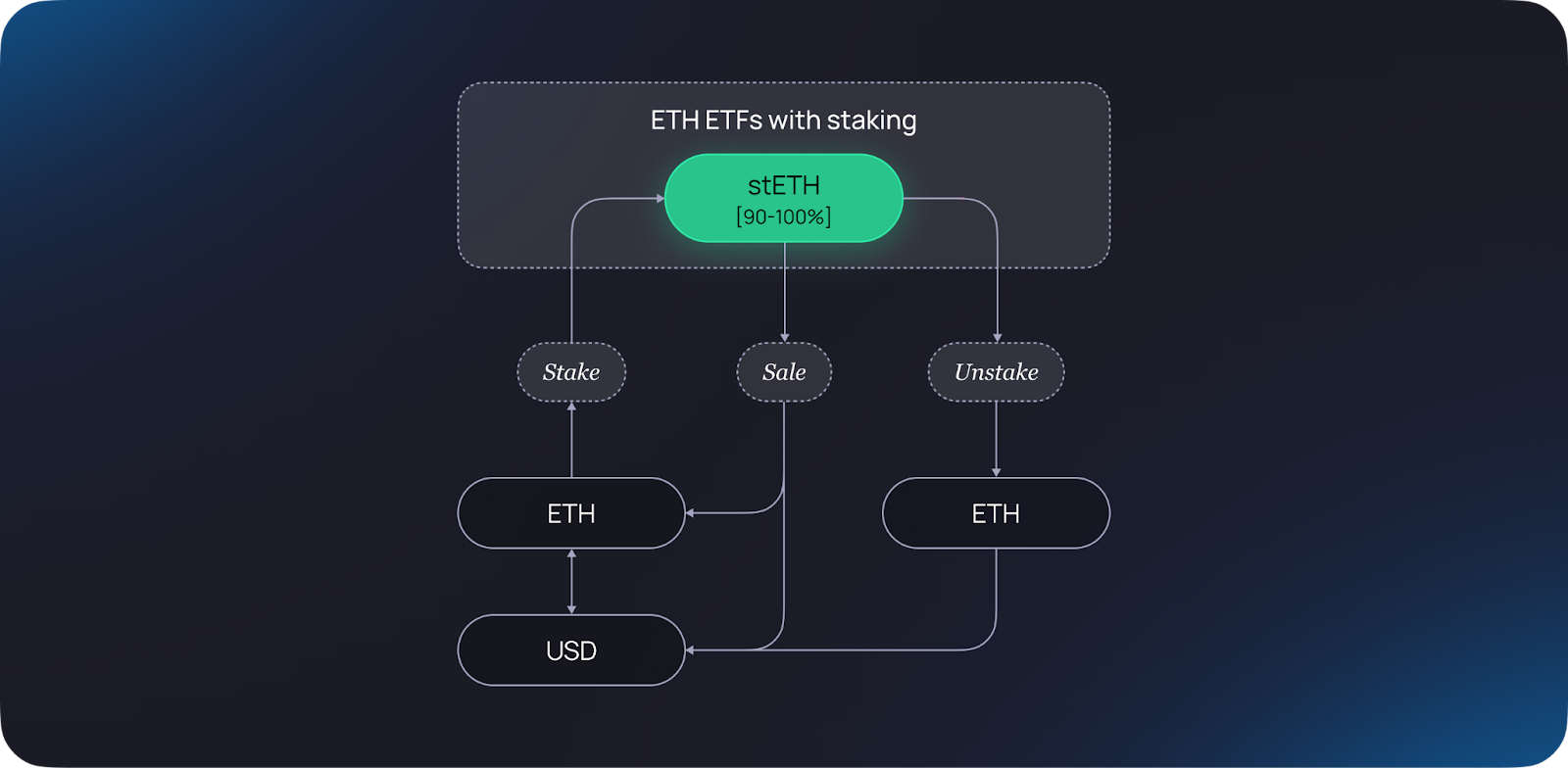

Liquid staking can help address some of these constraints by making staked ETH liquid.

When ETH is staked through the Lido protocol, users receive stETH, a liquid token designed to represent the staked position and the associated staking rewards generated. Because stETH is transferable, it can be traded, transferred, or used across secondary markets and DeFi applications while maintaining exposure to the underlying staking position.

This structure reduces the need for ETF and ETP issuers to start and stop validators every time fund flows change. Participants such as market makers can source stETH in secondary markets, allowing creations and redemptions to rely on available market liquidity instead of waiting for ETH to move in or out of validator queues.

In simple terms, liquid staking removes much of the operational burden of staking and turns it into a token the ETP issuer can work with. But this only works if the liquid staking token itself has the scale, liquidity, custody support, and pricing required for an exchange-traded product.

Why stETH Works for Institutional Products

Not every liquid staking token is suitable for an exchange-traded product. It needs scale, liquidity, custody support, reliable pricing, and enough market infrastructure for issuers and market makers to use it with confidence.

stETH currently represents more than 9 million ETH staked, over $18 billion in total value locked, and nearly one quarter of all staked ETH on the network. It is also integrated across a broad range of trading, lending, and collateral venues, with approximately $100 million of liquidity within 2% depth, more than $2 billion in weekly trading volume, and roughly $10 billion used as collateral across DeFi and centralised platforms.

That matters because scale alone is not enough. For an exchange-traded product, the underlying virtual asset also needs day-to-day tradability, dependable liquidity, and the ability to move through third-party financing and collateral workflows. stETH already does that.

stETH also sits inside institutional workflows that ETF and ETP issuers already use. Institutional custody and infrastructure support is live across providers including Fireblocks, Copper, and BitGo. More than $4 million has been invested in security audits, and more than 650 node operators run validators via the protocol. That combination of custody access, validator diversification, and operating history matters when assessing whether the structure works in practice.

What This Means for the Next Generation of ETH ETFs & ETPs

The next generation of ETH wrappers will likely split into two categories: spot ETH exposure, and staking-enabled ETH exposure. For the second category, liquid staking is structurally better aligned with the wrapper than native staking.

Native staking still matters. It is simply better suited to use cases where direct validator control matters most. ETFs and ETPs are built around something different: daily tradability, scalable distribution, reliable pricing, and operational simplicity.

Europe has already seen this architecture implemented in publicly traded products. WisdomTree's stETH-backed ETP, live since December 2025 on Xetra, SIX, and Euronext, is the clearest example of this model. In the U.S., similar structures are still at the proposal stage.

For issuers designing staked ETH products, the infrastructure they choose will shape liquidity, operational simplicity, and long-term competitiveness. On those measures, stETH stands out for its scale, secondary market depth, institutional custody access, and broader market infrastructure.

ETF and ETP issuers evaluating staked ETH products can connect with the Lido Institutional team to discuss structure, custody, and implementation.

Note that this content is provided for informational purposes only and does not constitute financial, investment, legal, or tax advice. Nothing contained herein should be interpreted as a recommendation or solicitation to buy, sell, or hold any digital asset.

Past performance is not indicative of future results, and outcomes may vary.

Participation in blockchain networks, staking, or DeFi activities involves risks, including smart contract risk, market volatility, liquidity constraints, and potential loss of assets. Readers should conduct their own research and seek independent professional advice before engaging with any protocol or product mentioned.